Domestic Streamlined Offshore & Certification Form 14654

Streamlined Program Overview

The IRS streamlined program breaks down into two camps.

1. Streamlined Foreign Offshore Program (SFOP)

2. Streamlined Domestic Offshore Program (SDOP) - described herein

The key difference between these two programs is that the first requires the taxpayer to meet the non-residency test. This has nothing to do with citizenship, or whether you filed 1040 or 1040NR, or the physical presence test.

To qualify for the more lenient program (Option 1 - Streamlined Foreign Offshore) - the taxpayer must be outside of the U.S. at least 35 days in 1 of the last 3 years (both programs require 3 tax returns + 6 FBARs).

If the taxpayer was present in the US (did not meet the above test), then they would only be eligible for DSOP.

The primary benefit of both programs is amnesty from FBAR penalties, failure to file penalties, and accuracy-related penalties.

Streamlined Domestic Offshore Overview

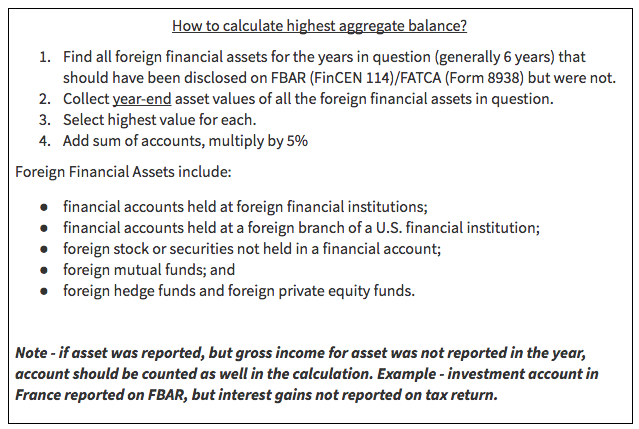

The latter program (SDOP) is less lenient, primarily in that it requires the taxpayer to agree to pay a penalty of 5% (Title 26 miscellaneous offshore penalty*) of the highest aggregated year-end balance of the taxpayers foreign financial assets during the years in question. In contrast, the streamlined foreign offshore program provides full amnesty from penalties.

Why file Domestic Streamlined Offshore (DSOP)?

For one, this program carries a capped risk - the 5% penalty described above. Secondly, provided that the examination results in a determination that the failure to file was not willful, the program still provides you with amnesty from draconian ‘Failure to file’ penalties, accuracy related penalties, and FBAR penalties. The program also caps the amount of years to file at 3 - without filing through one of the programs, the statute of limitations for prior years does not end.

Tax Returns, FBARs, and Certification (Form 14654)

The program requires the filing of the most recent 3 tax returns, along with any informational returns, and the 6 most recent FBAR reports. In addition, the taxpayer must prepare a certification letter (Form 14654), indicating that the non-compliance was not willful. This is more art than science, and you may enlist professional assistant to help tailor the statement.

The regular price for Streamlined Procedure services if purchased separately:

| 3 Years of Federal Tax Returns | 450 * 3 = $1,350 |

| 6 Years of FBARs | 85 * 6 = $510 |

| Analysis of situation and applicability for the program | $150 |

| Total | $2,010 |

|

We are offering a special package price of $1,450 - saving you 27%. |

|

|

Please note - the package above only consists of preparation & filing of the Tax Returns & FBAR. There is another form that is required. You can prepare it yourself or we can do it for you. |

|

| Preparation of the IRS Certification by U.S. Person Residing Outside of the U.S statement for the Streamlined Procedure costs | $300 |

| Preparation of the IRS Certification by U.S. Person Residing in the U.S statement for the Streamlined Procedure costs | $500 |